CARBON

We continue to inch higher in price, post the conclusion of coalition negotiations on Friday we have traded up at $71.75 this morning, all eyes now on next weeks final 2023 auction, most pundits suggesting another 'declined' auction result, no shortage of units on offer. NZX Managed Auction Service (etsauctions.govt.nz).

Industry commentary

Matt Cowie's latest LinkedIn post is worth a read, noting:

Friday’s big reveal of the coalition agreements between the National Party, NZ First and Act offered only very limited insight into their plans for the New Zealand Emissions Trading Scheme (NZ ETS). National’s commitment in its pre-election manifesto to “no major ETS reforms” was reinforced in its agreement with NZ First to “stop the current review of the ETS system to restore confidence and certainty to the carbon trading market”. There was no mention of the NZ ETS in the National-Act coalition document.

EU

- European carbon prices posted a marginal advance on the day and week, after earlier increases had given rise to speculation that the month-long decline fuelled by speculative selling may have come to an end as the expiry of the December contract approaches, while energy markets also ended little changed after a late decline on an uncertain weather outlook.

- Friday's close was at $136.50 NZD approx.

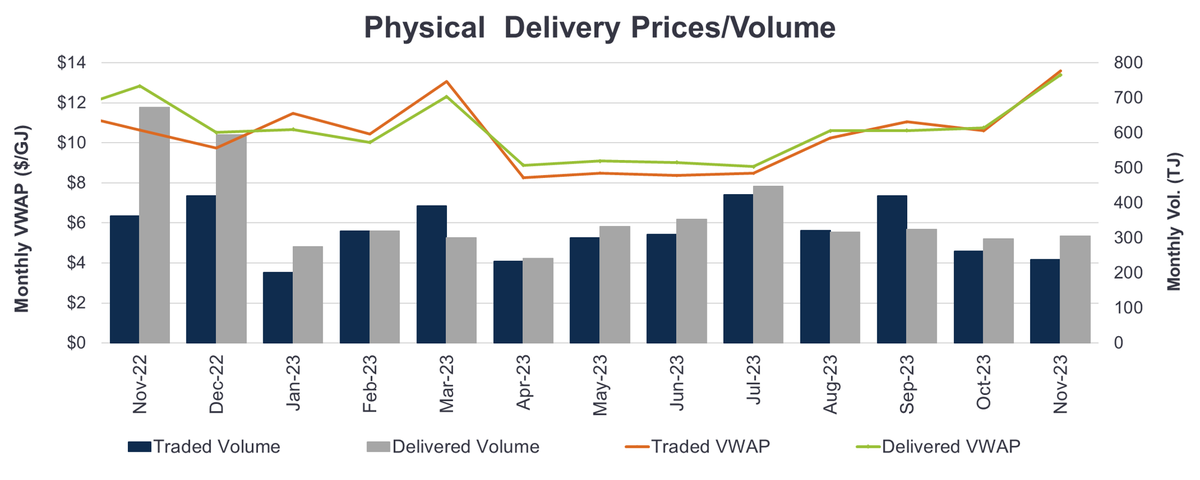

NATURAL GAS

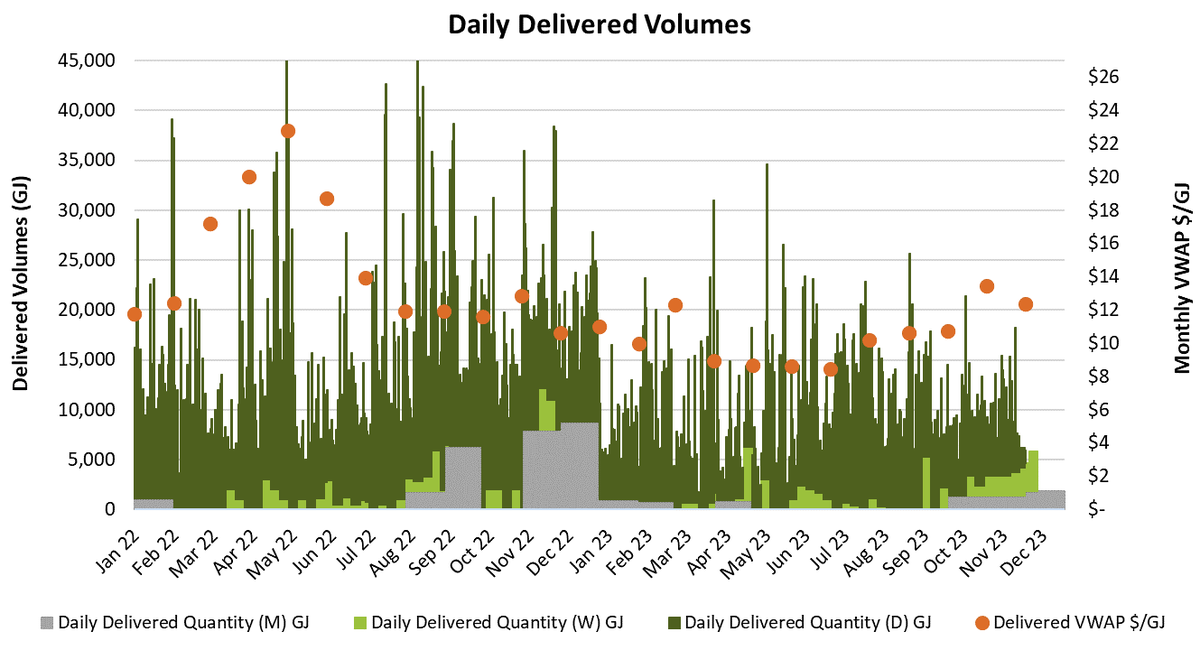

- Traded gas volume was well down on the previous week, dropping 70% to 33 TJ.

- Delivered gas volume also fell last week, down 19% to 71 TJ.

The System Operator made up 32% of traded volume, active on 3 days, buying all week, again underpinning the market prices.

- Traded price range was $12.50-$21.00.

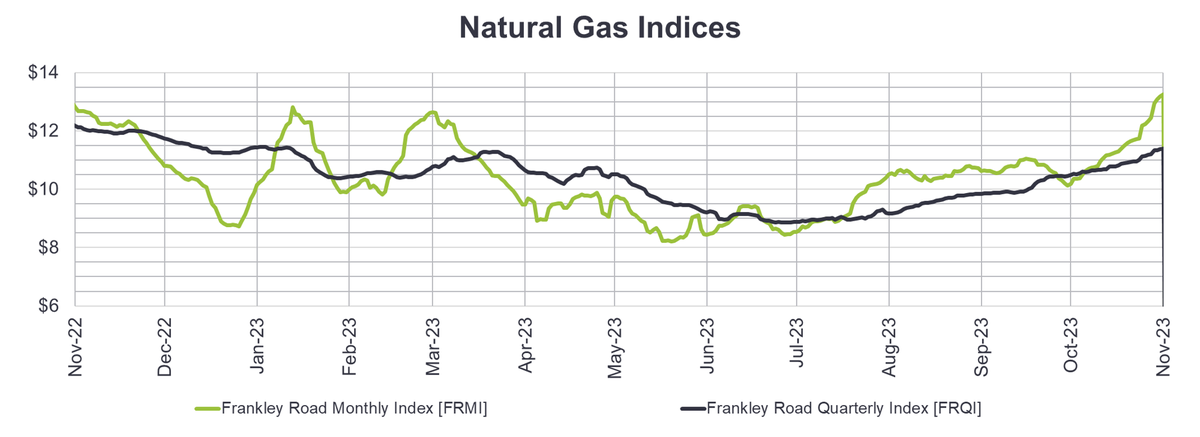

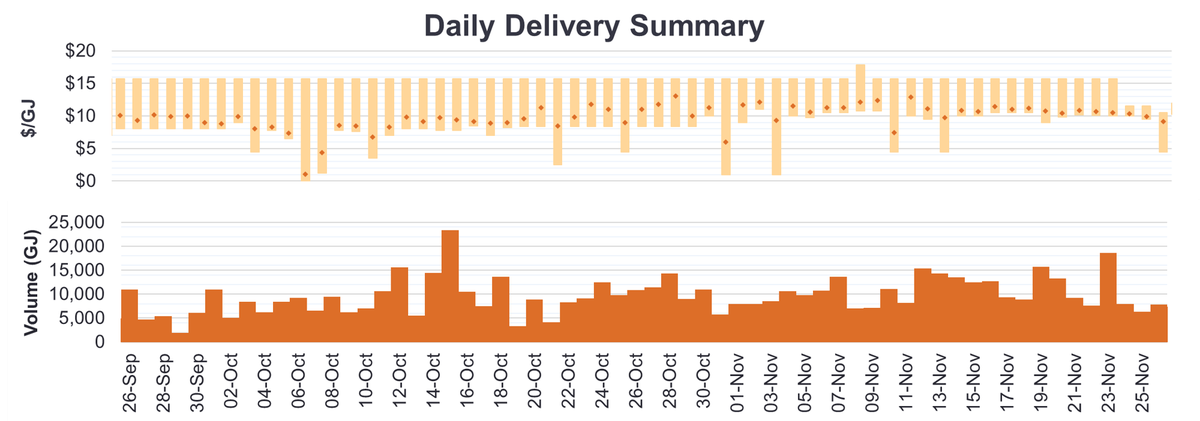

- Delivered VWAP rose 17% to $14.52.

- Traded VWAP rose 22% last week to $16.55

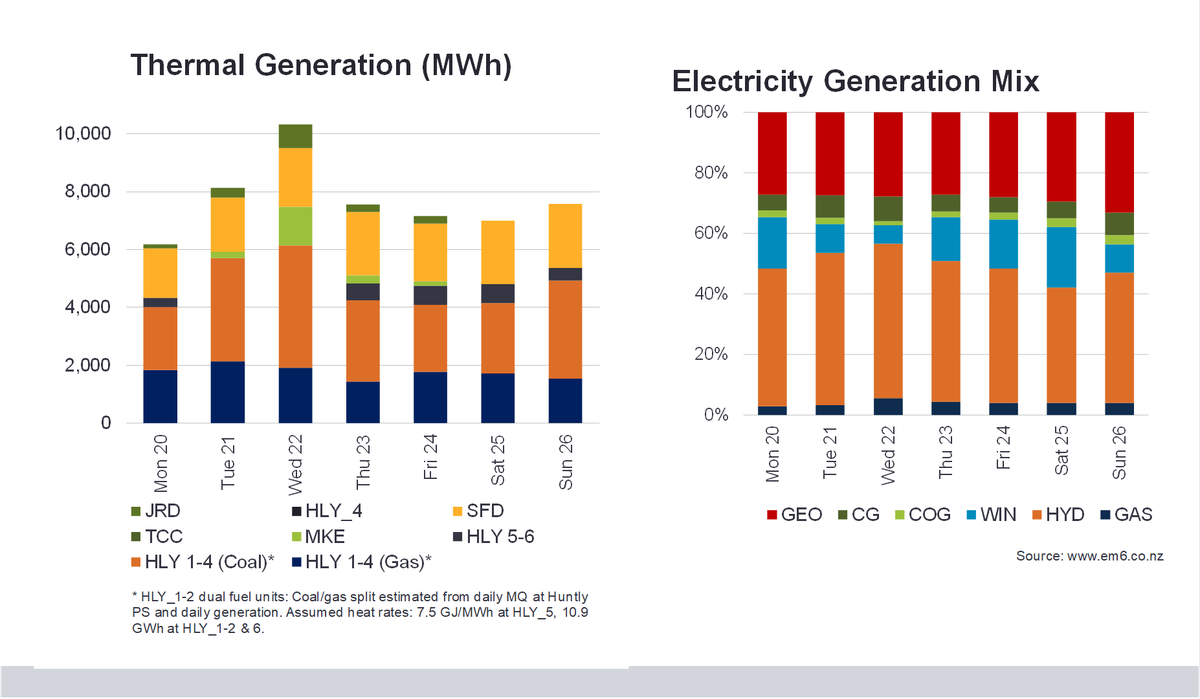

Gas as a portion of the electricity generation rose last week, making up 3.9% of the mix.

- Average electricity prices rose 18% in both Islands, the North Island averaging $147.67, whilst South Island prices averaged $141.59.

- Hydro storage fell 4% to 97% of average